The fast growth of the CBD industry has created opportunities and uncertainties when it comes to banking for CBD businesses.

Though the consumer demand for hemp-derived products keeps increasing, entrepreneurs are entering the market at an unprecedented speed. However, despite such growth, many CBD companies still struggle to access reliable merchant account services, payment processing solutions, and traditional banking support.

This struggle of CBD companies shows one of the biggest challenges in the CBD industry today and that is financial accessibility. There are also many challenges like regulatory uncertainty, compliance concerns, and the association between CBD and cannabis.

Even while hemp-derived CBD is legal in many regions, banks remain cautious due to strict compliance requirements, anti-money laundering(AML) regulations, and changing legal frameworks.

As a result, CBD businesses are often categorized as high-risk merchants that makes it difficult to secure stable banking relationships.

Hence, the main question for CBD becomes:

Will banks eventually adapt and fully support this growing sector? Due to advancements in fintech solutions, improved risk management tools, and increasing clarity around CBD regulations, the CBD market is slowly changing.

More banks have begun to explore CBD-friendly services that indicate a shift in customer perception.

This blog will walk you through whether traditional banks will fully adopt the CBD market, examine the challenges, opportunities, and future trends shaping CBD payment processing, CBD merchant accounts, and the broader financial ecosystem.

Also Read: How to Open CBD Business Bank Account

Understanding the CBD Industry

CBD(cannabidiol) is a naturally occurring compound that is derived from the hemp plant, which is a variety of cannabis that contains low levels of THC which is the psychoactive element which is responsible for the “high”.

Unlike marijuana which is a hemp-derived CBD that is widely accepted as non-toxication and is legally permitted in many countries. In the United States, CBD became federally legal under the 2018 Farm Bill, provided if the THC levels remain below 0.3%.

The CBD industry has now grown quickly and now spans across several major sectors:

- Wellness and supplements – It includes oils, capsules, and health-focused products

- Skincare and beauty – It includes creams, serums, and cosmetics infused with CBD

- Food and beverages – It includes edibles, drinks, and infused snacks

- Pet care – It includes CBD treats and oils for animal wellness

- Pharmaceuticals – Limited use in approved medical treatments

Despite its growing market and legal permission, CBD still operates in a regulatory gray area. Some of the concerns around CBD products include product labeling, health claims, and interstate commerce which creates uncertainty.

Due to lack of consistent regulations, banks remain cautious while dealing with CBD businesses.

Also Read: CBD Industry Trends Challenges and Future Outlook

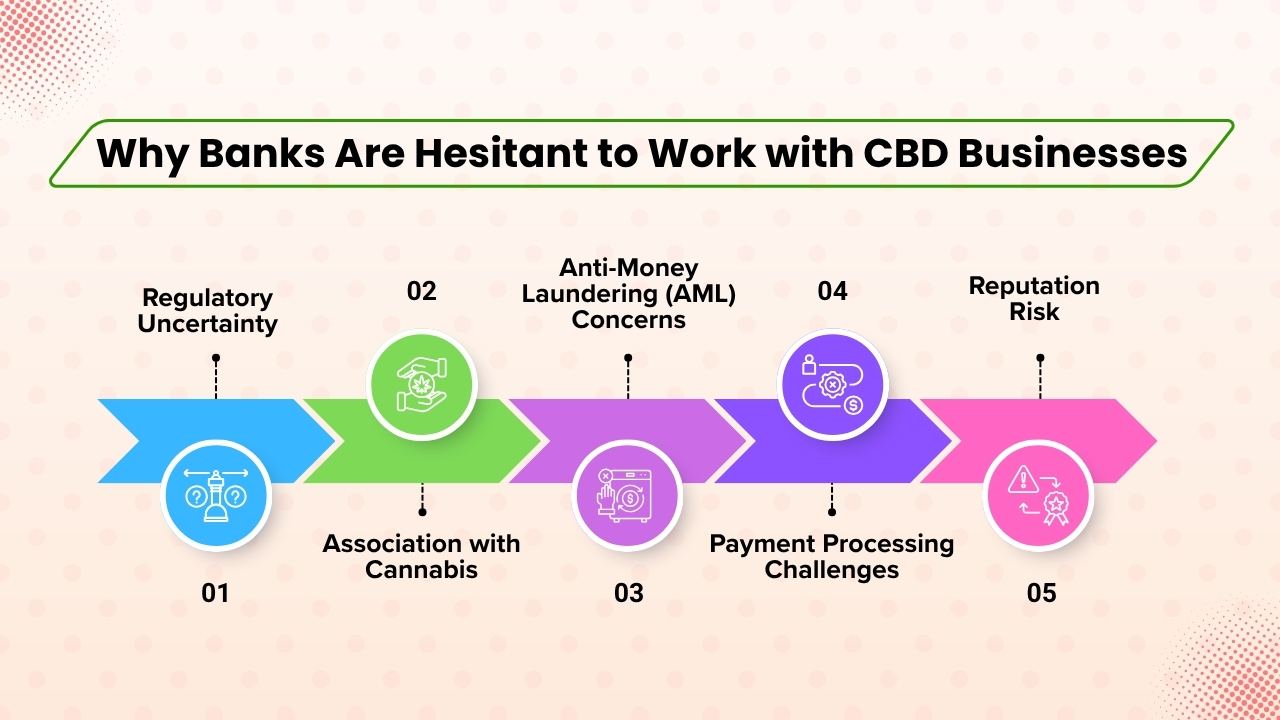

Why Banks Are Hesitant to Work with CBD Businesses

1. Regulatory Uncertainty

One of the biggest reasons why banks hesitate to work with CBD businesses is due to lack of clear and consistent regulations. Though CBD is legal in many regions, the rules surrounding CBD production, sale, and distribution are still changing.

Different government agencies may interpret laws differently that creates confusion for both businesses and banks. Banks operate under strict compliance so they have to ensure that they follow every regulation clearly.

If banks have any confusion regarding regulations then they may be exposed to serious risks such as regulation penalties, potential loss of banking licenses, or legal complications.

Any confusion increases their exposure to serious risks like regulation penalties, potential loss of banking licenses, or legal complications. As banks are highly tracked, even a small compliance error can lead to significant consequences.

For banks, unclear or changing laws make CBD businesses unpredictable, and uncertainty is often considered high risk by the banks.

Also Read: Guide to Start a CBD Business

2. Association with Cannabis

Although CBD is derived from hemp and is non-psychoactive, it is closely associated with cannabis that remains restricted or illegal in many regions.

Such a link often creates both reputational and compliance concerns for banks. Many banks can not clearly differentiate between CBD and marijuana, which lead them to categorize CBD companies as high-risk or cannabis-related businesses.

As a result, CBD merchants are often grouped into restricted industry lists which is similar to gambling. Such high risk classification often causes sudden account closures, rejected applications, or limited financial services.

Even though CBD businesses operate fully within the law, because of its connection to cannabis makes banks cautious as they want to avoid any regulatory scrutiny or any damage to their brand image.

Also Read: How to Market Cannabis

3. Anti-Money Laundering (AML) Concerns

Banks have to follow strict Anti-Money Laundering(AML) regulations which involve tracking bank transactions and verifying the validity of funds. For CBD businesses, these processes become more duplex.

It is essential for companies to prove that their products are derived from legally grown hemp and comply with all valid laws.

If there is no proper documentation then banks may fear that funds could be connected to illegal cannabis activities. Due to which it becomes essential for banks to track transactions closely, verify sources of income, and must report any suspicious activities to authorities.

Due to such scrutiny banks require additional time, resources, and expertise. As a result banks working with CBD businesses often require improved due diligence, which makes them more expensive and time-consuming for banks to manage. Most banks prefer to avoid all these additional challenges altogether.

Also Read: Why CBD Business are Considered High-Risk

4. Payment Processing Challenges

CBD businesses often face important challenges when it comes to payment processing. Transactions may get declined, flagged as suspicious, or blocked entirely by traditional payment gateways.

Additionally, CBD merchants often experience high chargeback rates which increases risk for payment processors and banks. Most mainstream banks are not willing to support CBD transactions, which forces businesses to depend on high-risk merchant accounts, offshore payment solutions, or alternative payment methods.

But such options often have higher fees, stricter terms, and less reliability.

The lack of stable payment infrastructure creates inconsistent cash flow and operational challenges for CBD businesses. For banks, such instantly adds more risk, which makes them less likely to offer support.

Also Read: Secure Payment Processing for CBD Ecommerce

5. Reputation Risk

Reputation is crucial in banking decisions. Banks are sensitive to the way their clients and services are viewed by regulators, investors, and the public.

Though CBD is legal in many regions, some stakeholders still consider CBD negatively due to its link with cannabis. Banks may have concerns regarding the possible reactions from their traditional customers, increased regulatory oversight, and misunderstandings among the general public.

Such perceived risk may impact a bank’s brand image and trustworthiness. As a result, many banks consider avoiding working with CBD businesses altogether rather than risking any negative publicity.

Until perception of the public fully aligns with the legal status of CBD, reputation concerns will continue to influence banking decisions.

Also Read: What is a High-Risk Merchant Account & Why CBD Needs One

The Current Banking Landscape for CBD Businesses

Despite challenges, the situation around CBD businesses is improving.

What’s Changing?

Several positive changes are shaping the future of CBD banking. Some banks are now providing CBD-friendly business accounts that allow companies to manage finances more reliably.

Additionally, specialized banks and fintech companies have entered the market that focuses on high-risk industries like CBD.

Payment processors are also changing, creating CBD-specific payment solutions that reduce transaction declines and improve approval rates.

At the same time, regulatory clarity is improving in crucial markets which helps banks to better understand compliance requirements and reduce uncertainty.

Also Read: Comparing CBD Payment Gateways

Types of Financial Support Available Today

CBD businesses now have access to a range of financial services, although often with limitations. These include:

- High-risk merchant accounts for processing card payments

- Limited business banking services like checking accounts

- Specialized lending options customized for high-risk industries

- Alternative payment methods, including ACH transfers and, in some cases, cryptocurrency

However, these approaches have certain compromises.

CBD businesses usually face high transaction fees, stricter onboarding processes, and detailed documentation requirements. Additionally, CBD accounts are subject to ongoing monitoring and compliance checks that makes banking more complex than in traditional industries.

Though the progress is evident, full integration into mainstream banking is still evolving.

Also Read: Why Every CBD Business Needs a Customized POS System

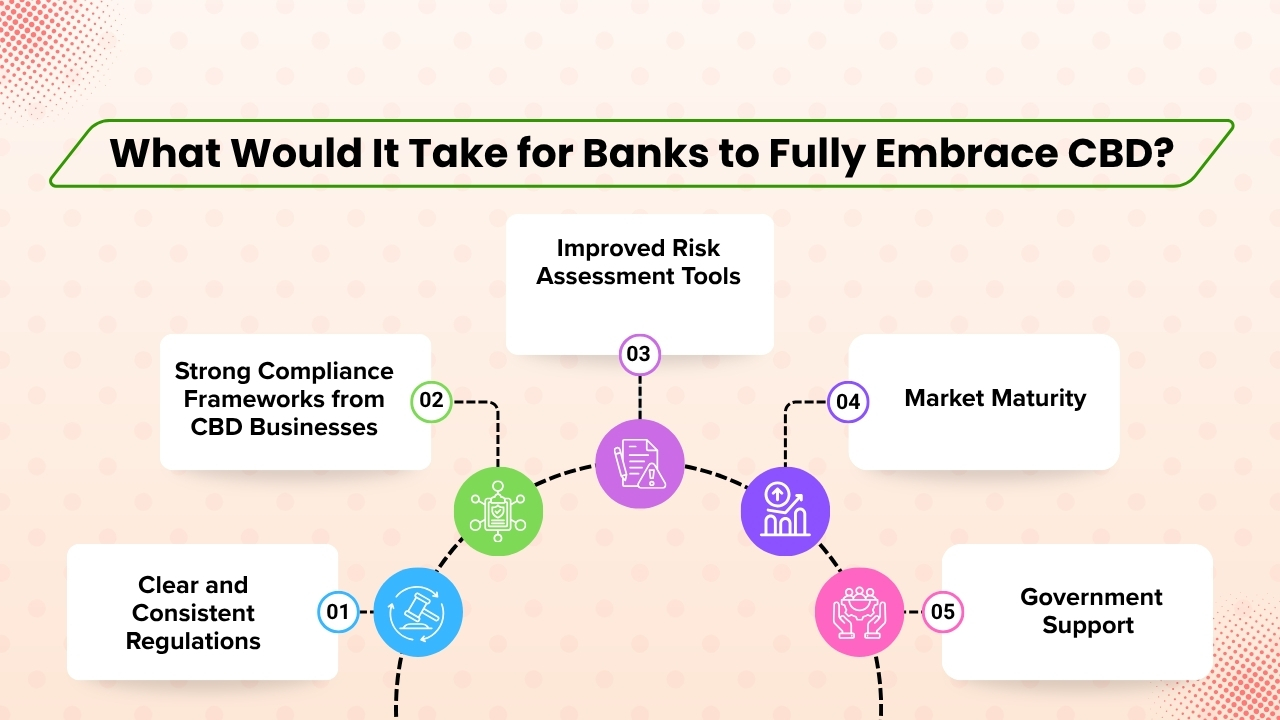

What Would It Take for Banks to Fully Embrace CBD?

For banks to fully adopt CBD businesses, several important changes should take place across regulatory, operational, and industry levels. Though the progress is already being made, wide acceptance of CBD businesses by banks will depend on reduced risk, increased transparency, and building trust between banks and CBD companies.

1. Clear and Consistent Regulations

One of the most crucial factors is the establishment of clear and consistent regulations. Banks require well-defined national and international guidelines which remove confusion around CBD legality.

It is essential to have clear definitions regarding what qualifies as a legal CBD product, along with standard compliance requirements which businesses must follow.

When regulations around CBD products are steady and uniformly enforced, banks can confidently associate with CBD businesses without the fear of sudden legal changes or penalties. Clear regulations work as the foundation for trust and long-term bank associations.

Also Read: How Zero-Processing Works For CBD Business

2. Strong Compliance Frameworks from CBD Businesses

CBD companies themselves play a crucial role in gaining banking acceptance. Businesses must demonstrate strong compliance practices that include transparent supply chains that clearly trace the origin of hemp products.

It is also essential to verify THC levels to prove that products meet legal standards. Additionally proper licensing, accurate documentation, and compliant labeling helps to build credibility.

When a CBD business is more transparent and organized then lower the perceived risk for banks. And companies which prioritize compliance are more likely to secure stable banking relationships.

Also Read: How to Protect Your CBD Business From Payment Processor Shutdowns

3. Improved Risk Assessment Tools

Advancements in technology helps banks to manage the risks associated with CBD businesses. Banks are mostly investing in advanced fraud detection systems, AI-driven compliance monitoring, and industry-specific risks.

These tools help businesses to analyze transactions effectively, find suspicious activity, and ensure ongoing compliance. Having data and smarter systems, helps banks to make informed decisions and reduces any chances of uncertainty, that makes CBD businesses more attractive and manageable clients.

Also Read: How AI is Changing Fraud Prevention in CBD Transactions

4. Market Maturity

As the CBD industry keeps growing and mature, it becomes more attractive to traditional banks. Due to increased consumer trust causes high demand for CBD products and more stable revenue streams.

At the same time, product quality improves when companies adopt better manufacturing and testing standards. Regulatory bodies have also become more organized, offering clearer rules and oversight.

Such overall evolution reduces volatility and places the CBD industry as a legitimate, long-term market that encourages banks to participate more actively.

Also Read: The Ultimate Guide to Social Media Marketing

5. Government Support

Government involvement is essential for closing the gap between banks and CBD businesses. Offering legal protections for banks while working with compliant CBD companies which can highly reduce risk concerns.

With clear guidance from regulators banks help to understand how to operate CBD businesses within the law, while regular enforcement ensures fairness and consistency across the CBD industry.

Without strong government banking, banks are likely to remain cautious. But supportive policies help banks to feel more confident growing their services to CBD businesses.

However, full banking acceptance of CBD businesses requires regulation clarity, strong compliance, technological advancement, industry maturity, and government support.

When all these elements come together then the path toward mainstream bank integration will become increasingly achievable.

Also Read: State by State Guide to Selling CBD Online and In-Store

The Role of Payment Technology in Bridging the Gap

Technology is playing a crucial role in filling the gap between banks and CBD businesses by resolving many of the risks that have traditionally reduced financial access.

While the CBD industry keeps growing, innovative payment technologies are helping to create a more secure, transparent, and compliant financial ecosystem.

Several key innovations are driving this transformation:

- Fintech platforms which offer CBD-friendly payment solutions that allow businesses to process transactions more reliably without frequent disruptions.

- Blockchain technology improves transparency by enabling secure tracking of the entire supply chain, which ensures that products are sourced from legal hemp and also meet regulatory standards.

- Digital identity verification systems help to confirm the legitimacy of businesses and customers, which reduces fraud and improves trust.

- Automated compliance tools simplify regulatory processes by continuously tracking transactions and ensuring that they adhere to legal requirements.

Such advancements highly reduce uncertainty for financial institutions. Improving transparency, strengthening compliance, and reducing fraud risks, payment technology is making CBD businesses more trustworthy and easier to manage.

As a result, banks are becoming more open to working with the CBD industry, which makes way for broader financial inclusion.

Also Read: How Fast Payouts Can Improve Your CBD Business Cash Flow

Opportunities for Banks in the CBD Industry

1. New Revenue Streams

Banks that choose to work with CBD businesses may find crucial new revenue opportunities. Since CBD companies often face limited banking options, they are willing to pay premium fees for reliable and compliant financial services.

It includes higher processing fees, account maintenance charges, and compliance-related costs. For banks, association with CBD businesses creates a profitable niche market with less competition.

By providing customized solutions for CBD merchants, financial institutions can tap into a reliable revenue stream while supporting a market that is often overlooked. As demand for CBD products keeps increasing, transaction volumes are also expected to increase, further increasing revenue potential.

Also Read: How Much Does an Average CBD Store Make

2. Market Differentiation

When banks early adopt CBD businesses helps banks to have a competitive advantage in a highly competitive banking market. Though many traditional banks remain hesitant, many forward-thinking banks can position themselves as adaptable.

Banks that support CBD businesses show a willingness to adopt emerging industries and evolving market trends. It not just improves brand reputation but also attracts high-growth sectors which face similar challenges.

When banks become leaders in CBD financial services, banks can build a strong identity as progressive banks which support modern businesses.

Also Read: Marketing Ideas for CBD Business

3. Long-Term Growth Potential

The CBD industry is expected to experience considerable growth in the coming years due to increasing consumer demand, expanding product categories, and wider acceptance.

While the market matures, CBD businesses will require more advanced financial services that include lending, expansion funding, and international transaction support.

Banks that establish relationships early with CBD businesses can benefit from long-term partnerships while these businesses grow. It creates opportunities for sustained growth and recurring revenue.

Banks that invest in the CBD sector today position banks to capitalize on a quickly growing market in the future.

Also Read: How to Create an Effective CBD Business Plan

Challenges That May Persist

While the CBD industry continues to evolve and gain wider acceptance, there are many challenges which are likely to remain and slow down full banking adoption.

One of the primary issues with CBD businesses is the ongoing regulatory variations across different regions. Different countries and states have their own rules regarding CBD that makes it difficult for banks to apply a uniform compliance strategy. Frequent regulatory updates further add to the complexity.

Another challenge associated with CBD businesses is the continuous stigma associated with cannabis related products. Though CBD is non-psychoactive, its connection to cannabis still creates hesitation among regulators, banks, and certain customer groups. This perception can impact decision-making by the banks.

Additionally, differences in product quality and compliance standards remain a concern. All CBD businesses do not follow strict guidelines that increase the risk of non-compliant products that are entering the market. Such inconsistency makes banks more cautious.

Also Read: CBD & Crypto Payments

Global Perspective: CBD Banking Around the World

1. United States

In the United States, CBD is legal under federal law with specific restrictions especially when CBD is derived from hemp and contains low THC levels.

However, banking access for CBD businesses is still inconsistent. Some banks are willing to work with the industry, while other banks remain cautious due to compliance concerns and changing regulations. It creates a mixed environment for CBD entrepreneurs.

2. Europe

Europe has more varied restrictions because CBD regulations are different from country to country. In most places of Europe, the CBD market is more open than other places and CBD businesses may get better bank support.

However, banks still function under strict regulatory oversight that means access to banking services can depend highly on local laws and product classifications.

3. Asia

Asia remains highly restrictive for CBD and cannabis-related products. In most Asian regions, legal limitations and strict government controls make it very difficult for CBD businesses to operate, let alone secure banking services.

As a result, the banking sector for CBD businesses in Asia is far less supportive than in Western markets.

4. Canada

Canada has a more established cannabis framework, that makes banking support for CBD businesses comparatively stronger. Banks are generally more familiar with the industry and are more equipped to manage its risks.

Such global differences show the increasing need for harmonized regulations worldwide.

Also Read: How to Open a CBD Dispensary in California

The Future of CBD Banking

The future of CBD banking is constantly changing, with clear signs of progress across the financial sector. Though banks may not immediately accept CBD businesses, the overall development is positive while the regulations improve and industry confidence grows.

1. Short-Term Outlook

In the short term, CBD businesses will continue to witness gradual improvements in banking access. Most banks have started to explore CBD-friendly services, but many other banks will still remain cautious.

As a result, CBD businesses will mostly depend on specialized providers like high-risk merchant account services and fintech platforms. Such solutions will help to maintain operations, but still involve higher fees and stricter compliance requirements.

2. Mid-Term Outlook

Over the mid-term, the CBD sector is expected to become more stable and accessible. Mid-sized banks are mostly to enter the market when regulatory clarity improves and risk management tools become more advanced.

This phase will provide better payment processing solutions, which reduces transaction failures and improves customer experience. Due to the increased competition among service providers may cause more favorable pricing and flexible options for CBD businesses.

3. Long-Term Outlook

In the long term, CBD banking is expected to reach mainstream banking acceptance. While regulations become standardized and the industry matures, CBD businesses will be considered similarly to other legal industries.

Banks will start offering fully integrated bank services, which includes loans, payment processing, and treasury solutions without labeling CBD as high-risk. It creates a more stable and scalable environment for growth.

Overall, CBD businesses with banks in the future looks promising, while progress will be gradual rather than immediate, which requires continuous collaboration between regulators, banks, and CBD businesses.

Conclusion

The question of whether banks will fully adopt CBD businesses is not just a matter of possibility, but one of timing and progression. The CBD industry has already proved to be a business with economic potential, and while consumer demand continues to increase, banks are gradually knowing the value of supporting this sector.

However, challenges like regulatory uncertainty, compliance complexities, and stigma still prevent immediate, widespread adoption.

Encouragingly the CBD sector is evolving. Improvements in regulatory clarity, advancements in fintech solutions, and stronger compliance practices among CBD businesses are helping to reduce the risks that once made banks hesitant.

At the same time, governments and regulations are beginning to provide clear guidance which is essential for building confidence within the financial system. These changes are creating a more stable environment where banks can explore opportunities without excessive exposure to risk.

In the long run, CBD businesses are likely to become a standard part of the banking ecosystem. While as the industry matures and regulations become more consistent, banks will shift from cautious participation to full integration. This will cause better access to financial services, lower costs, and increased growth opportunities for CBD companies.

Ultimately, full acceptance of banks for CBD businesses will not happen overnight, but the direction is clear. With continuous collaboration between regulators, banks, and CBD businesses, the gap will continue to close, paving the way for a more inclusive and sustainable financial future.

If you still have any query about whether banks will ever fully embrace CBD businesses then you may write to us at CBD Merchant Solutions and we are more than happy to assist you.

Frequently Asked Questions (FAQs):

1. Is CBD legal for banking purposes?

CBD derived from hemp due to low THC is legal in many countries, but banking regulations often lag behind that makes banks cautious about offering services.

2. What services are hardest for CBD businesses to access?

Merchant accounts, payment processing, loans, and credit lines are the most difficult services to secure due to higher perceived risk.