AI is transforming the fraud prevention implementation in CBD transactions which helps merchants to stop any risk activity without slowing any legitimate customers.

As CBD products are becoming more mainstream, shoppers expect the same fast, smooth checkout experience which they get from other major retailers like tap-to-pay, in-store, mobile wallet, and recurring billing for subscriptions.

But as CBD is often labelled as high-risk category, merchants face stricter oversight from banks and processors, which makes fraud prevention, chargeback reduction, and payment compliance crucial for long-term stability.

Traditional rule-based systems struggle to match the speed and complexity of today’s fraud landscape because of card-not-present attacks, account takeovers, card testing, and friendly fraud now evolve quickly across mobile-first eCommerce and subscription checkouts.

AI-fraud detection uses machine learning to analyze real-time signals like device fingerprints, behavioral patterns, transaction velocity, geolocation, and customer history to assign smarter risk scores and choose the right outcome like approve, step up verification, or block.

The result is fewer false declines, higher payment approval rates, and stronger revenue protection without slowing down checkout for legitimate customers.

For CBD merchants, AI enhances security by combining tokenization and encryption with real-time risk checks to protect payment data and lower the chances of disputes.

Many CBD-friendly processors now integrate AI with compliance-first controls, such as SKU-level monitoring and region-based restrictions, to prevent processor issues before they happen.

As the CBD market grows more competitive, brands that combine fast checkout with AI-powered risk management gain an advantage like higher conversions, fewer chargebacks, stronger trust, and more reliable payment processing.

Also Read: How to Protect Your CBD Business from Payment Processor Shutdowns

Why CBD payments attract more scrutiny (and how that affects fraud)

Fraud is a cost of doing business in nearly every online industry, but CBD payments are placed under higher scrutiny by banks and payment processors.

CBD payment scrutiny comes less from fraud assumptions and more from the reality that compliance rules shift, reputational risk is higher, and the financial downside for processors is greater if something goes wrong.

As a result, even small increases in fraud or disputes can lead to outsized consequences for CBD merchants.

CBD payment scrutiny comes less from fraud assumptions and more from the reality that compliance rules shift, reputational risk is higher, and the financial downside for processors is greater if something goes wrong.

As a result, even small spikes in fraud or disputes can lead to outsized consequences for CBD merchants.

One of the biggest drivers of scrutiny is regulatory complexity. CBD laws vary widely by jurisdiction, with different rules around THC thresholds, product labeling, sourcing, and allowable claims.

What is compliant in one state may be restricted or outright prohibited in another. Payment processors must ensure they are facilitating transactions that violate local or federal guidance, which means they apply stricter monitoring to CBD transactions at every phase of the payment flow. From a risk perspective, uncertainty equals exposure, and exposure demands tighter controls.

Another factor is reputational and policy risk. Banks and acquiring institutions favor merchant portfolios which are stable, predictable, and unlikely to attract regulatory or media attention.

Despite its growing mainstream acceptance, CBD is still classified as a higher-variance category. Policy changes, enforcement actions, or public scrutiny can quickly shift how CBD is treated, and processors are highly sensitive to those changes.

To protect themselves, they often enforce more conservative thresholds around approvals, transaction patterns, and ongoing account reviews.

Chargeback sensitivity also plays an important role. In higher-risk verticals, dispute ratios are watched more closely. A chargeback rate that might be manageable in traditional retail can trigger alerts, reviews, or penalties much faster for CBD merchants.

Friendly fraud, subscription confusion, delayed fulfillment, or unclear refund policies can all contribute to disputes even when no malicious fraud is present.

Because disputes are costly and indicate potential compliance gaps, processors react quickly to keep risk contained.

The practical impact for CBD merchants is that fraud and disputes have faster, more severe consequences. Sudden fund holds, rolling reserves, delayed settlements, or even processing interruptions can occur with little warning if risk limits are crossed.

These actions are often preventative, designed to limit exposure before problems escalate.

This is why the objective for CBD businesses extends beyond basic fraud prevention. Success depends on managing fraud, disputes, and compliance hygiene simultaneously, while maintaining consistent approval rates and transaction stability.

Merchants that invest in transparent product data, clear customer communication, compliant checkout flows, and intelligent fraud controls are better positioned to operate smoothly earning processor trust while protecting revenue in a highly scrutinized payment environment.

Also Read: Secure Payment Processing for CBD Ecommerce

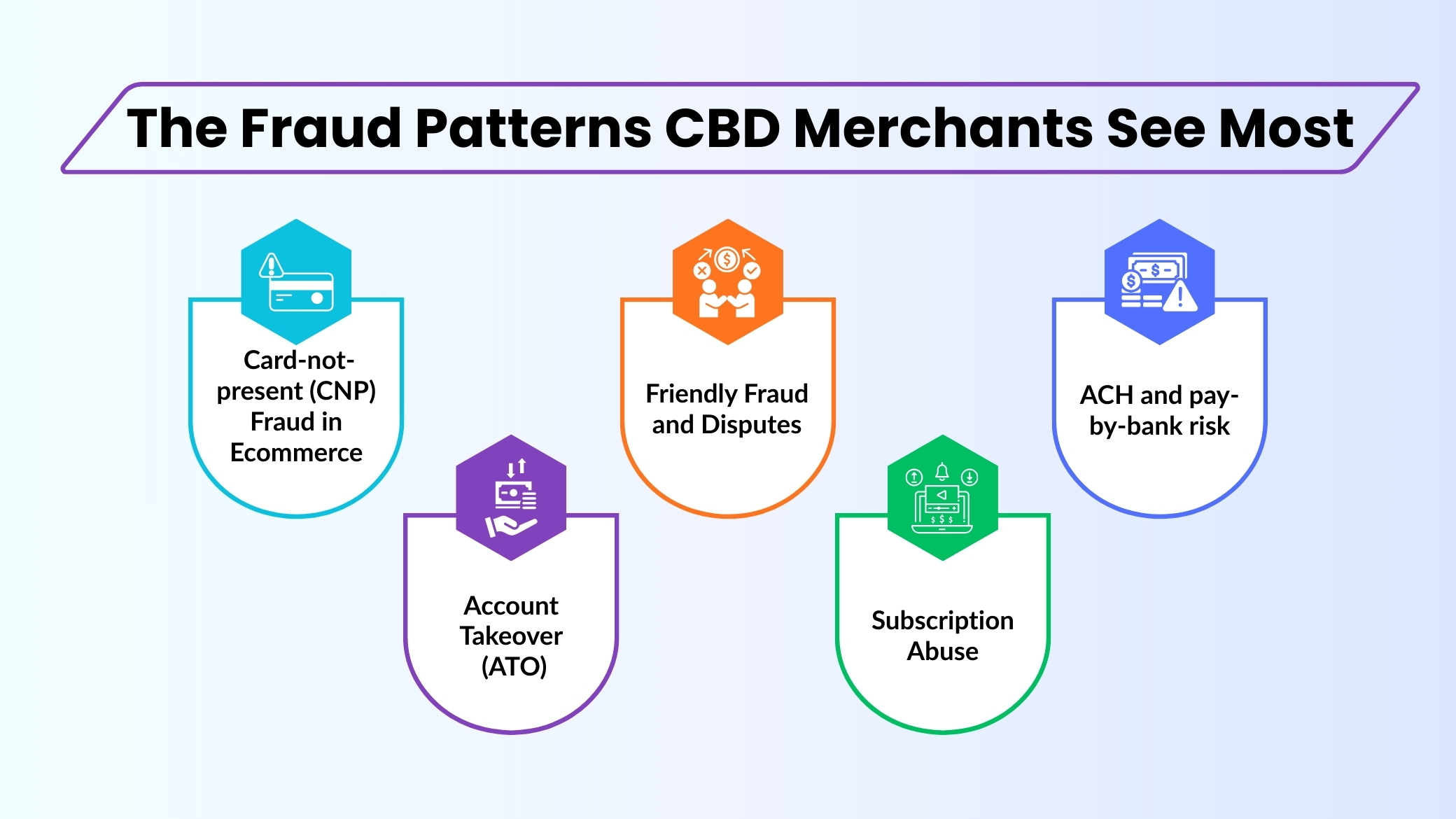

The Fraud Patterns CBD Merchants See Most

CBD merchants often face tighter processing monitoring, so even normal-looking anomalies can trigger reviews. Fraudsters exploit this by combining into legitimate traffic and shifting tactics quickly.

1. Card-not-present (CNP) fraud in ecommerce

Stolen card details are commonly “tested” at checkout using small authorizations or low-value purchases(card testing). Once a card is confirmed valid, fraudsters scale up to higher-value carts, faster shipping options and bulk orders often in short bursts from the same device, IP range, or bot network.

Also Read: How to Integrate CBD Payment Solutions With Ecommerce Platform

2. Account takeover (ATO)

Fraudsters take over legitimate customer accounts often using stolen login data or automated credential-stuffing attacks and then place rapid repeat orders using the cards already saved on file.

Common indicators include sudden login location changes, new device fingerprints, shipping address edits, and unusually fast checkout behavior after login.

Also Read: CBD Merchant Account Vs Regular Merchant Account

3. Friendly fraud and disputes

Chargebacks can come from customers claiming the purchase was not authorized, they don’t recognize the descriptor, or the product “never arrived”.

Unclear billing descriptors, slow deliveries, and weak post-purchase communication can increase chargebacks by making legitimate customers assume the transaction was fraudulent.

Also Read: How to Avoid Frauds and ChargeBacks in CBD Payment Processing

4. Subscription abuse

Recurring billing is attractive to fraudsters because it can generate ongoing revenue with less effort. They may sign up using compromised cards, then continue billing until the issuer or customer catches it. Risk increases when trials, discounts, or “first-month” promos are easy to exploit repeatedly.

5. ACH and pay-by-bank risk

ACH returns and disputes follow different rules than card chargebacks, but first-time bank debits, online transactions, and limited account verification still create meaningful exposure for merchants.

Look for mismatched identity signals, new bank accounts linked to high-risk behavior, and unusual return or NSF patterns.

Also Read: How to Open CBD Business Bank Account

Why AI matters (and rules alone aren’t enough)

Fraud tactics change fast. Attackers constantly shift order size, attempt frequency, device fingerprints, IP locations, and shipping behavior so they start blocking legitimate customers.

That’s why AI-based fraud prevention works better as it studies behavior across transactions, customer accounts, and full checkout sessions to detect subtle risk signals humans and static rules miss.

As it learns from outcomes like chargebacks and refunds, it adapts to new patterns, catching fresh fraud variants earlier while reducing false declines that frustrate real buyers.

Also Read: Email Marketing for CBD Business

Old-School Fraud Prevention vs AI-driven prevention

Old-school fraud prevention is mostly built on static rules like simple “if/then” checks that flag transactions when a pattern seems risky.

For instance, a merchant might block an order if the billing country does not match the shipping country, if the cart value exceeds a set threshold, or if too many payment attempts come from the same IP address.

These rules can be helpful for catching obvious abuse, especially early on, because they are easy to set up and straightforward to explain.

But rules-based systems have two major weaknesses. First, fraudsters learn them quickly. Once attackers recognize what causes blocks, they simply change tactics by splitting purchases into smaller orders, rotate IPs using proxies or replicate “normal” customer behavior.

Second, static rules often create false declines, which is a bigger problem than most merchants realize. Mobile shoppers often appear “inconsistent” because VPNs, switching between 4G/5G and Wi-Fi, and carrier routing can change IP and location indicates mid-checkout even when the purchase is legitimate.

A strict rule engine treats these situations as risk, even when the buyer is legitimate causing lost revenue and frustrated customers.

AI-driven fraud prevention takes a different approach like risk scoring with context. Rather than depending on a few hard limits, AI models evaluate many signals in real time.

These signals can include device and browser fingerprints, checkout speed, account history, shopping patterns, shipping behavior, email and phone consistency, and whether the transaction matches the normal behavior of the customer.

The result is not just approval or block. Many systems classify transactions in three categories: likely fraud, likely legitimate, and uncertain where step-up verification like 3DS, OTP, or additional checks can be applied.

Importantly, modern AI tools often optimize for business outcomes, and not just fraud blocks. They aim to increase approval rates, reduce false declines, and reduce chargebacks at the same time.

For CBD merchants, this balance is crucial as blocking too aggressively can reduce conversions, while approving too loosely can cause triggers, higher chargeback ratios, and greater scrutiny from processors.

Also Read: How Fast Payouts Can Improve CBD Business Cashflow

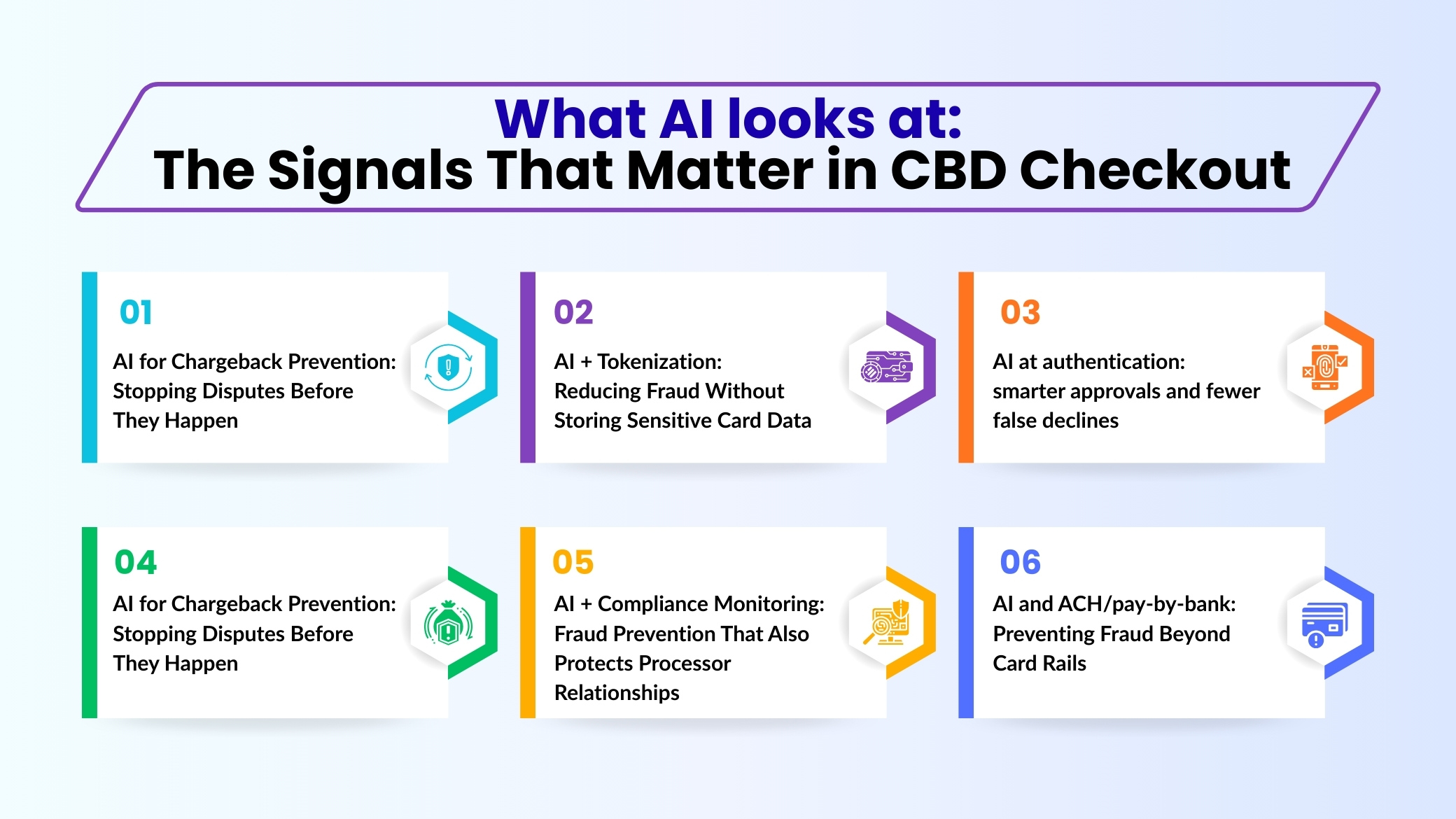

What AI looks at: the signals that matter in CBD checkout

AI-driven fraud prevention in CBD checkout works by analyzing patterns and not indicating warnings. These systems learn from behavior across your own store and depending on the provider from broader merchant networks to understand what normal looks like and where risks start to emerge.

One major category is device and session intelligence. AI evaluates whether a device fingerprint stays consistent with time or appears freshly generated on every visit.

Spotting emulators, rooted or jailbroken phones, browser tampering, and automation tooling helps reveal when a shopper is actually a scripted fraud attempt.

A consistent cookie trail indicates a genuine returning shopper, while constantly “fresh” sessions can indicate bots, device spoofing, or repeated fraud testing.

Behavioral signals help confirm intent by showing whether the shopper interacts like a real person or follows the repetitive, unnatural patterns typically of bots and fraud scripts.

AI models analyze typing speed and rhythm to distinguish human behavior from bots, along with mouse or touch movement patterns that show whether interactions are natural or scripted.

Time-to-checkout and navigation flow are also important because fraud often moves unnaturally fast or skips steps that real shoppers usually take.

Identity and customer history provide valuable context. Email quality and age can indicate risk especially when throwaway or recently created addresses are used.

By analyzing prior approvals, refunds, subscription timelines, and retry frequency, AI can distinguish reliable repeat buyers from accounts showing early warning signs of misuse.

On the transaction and product side, AI looks at basket composition. Certain product mixes may have higher resale or abuse risk, especially when combined with unusually large quantities or first-time buyer behavior.

High-ticket bundles from new customers often deserve closer scrutiny than repeat purchases of familiar items.

Finally, location and network signals help to find anomalies. When IP reputation is poor, billing and shipping are unusually far apart, or location signals show “impossible travel,” the transaction is more likely to be high-risk and may require verification.

Crucially, none of these signals alone should automatically block a sale. The real value of AI lies in how it combines them, learning which patterns predict chargebacks and which are simply normal behavior for your CBD customers.

1. Real-time decisions: “frictionless” when safe, “step-up” when needed

Real-time fraud decisions work best when they match the response to the risk level, rather than forcing every customer through the same challenges.

AI makes this possible by scoring each checkout in seconds and choosing the least disruptive action that still protects the merchant. This tiered approach is especially valuable for CBD businesses where unnecessary declines can hurt conversions, but missed fraud can cause disputes and added processor scrutiny.

For low-risk transactions, the ideal outcome is frictionless approval. With no extra steps, no delays, customers complete checkout like they would on any major ecommerce site.

These orders usually come from consistent devices, stable identity signals, normal cart behavior, and customers with clean history.

For medium-risk transactions, AI can cause step-up verification to confirm the buyer without impacting the sale. Common examples include a one-time passcode(OTP), quick identity confirmation, address verification prompts, or strong customer authentication flows where applicable.

The goal is to add just enough friction to separate legitimate customers from suspicious activity. For high-risk transactions, the safest response is block or manual review.

This is reserved for cases with multiple red flags like automation signals, unusual shipping changes, repeated payment attempts, or patterns linked to chargebacks.

The core principle is simple: apply friction only when the risk warrants it, so you reduce fraud while keeping checkout fast and conversion-friendly.

Also Read: CBD Industry Trends, Challenges and Outlook

2. AI + tokenization: reducing fraud without storing sensitive card data

Tokenization has become one of the most important advances in payment security, especially for merchants that handle repeat and online transactions.

Instead of storing or transmitting sensitive card details, tokenization replaces the primary account number(PAN) with a payment token which is a randomized value that has no meaningful use outside its intended context. This makes stolen data far less valuable to fraudsters.

In EMV payment tokenization, the real card number is removed from the transaction flow entirely and replaced with a token that can be tightly constrained.

Tokens may be limited to a specific merchant, device, channel, or transaction type, which significantly reduces their usefulness if intercepted. Even if attackers gain access to a token they usually can’t reuse it elsewhere like raw card data.

For CBD merchants, tokenization helps secure saved cards, subscription billing credentials, and mobile wallets transactions while minimizing direct exposure to sensitive data, reducing breach risk and easing compliance pressure.

Combined with AI fraud detection, tokenization adds strong fraud protection. AI flags risky behavior, tokenization reduces the damage if data is compromised, and checkout stays fast with fewer declines.

Also Read: Selling CBD Products Online

3. AI at authentication: smarter approvals and fewer false declines

Authentication is one of the most important factors in the payment flow because this is where perfectly legitimate customers can get declined for “looking risky”, especially in higher-scrutiny categories like CBD.

Today, networks and issuing banks increasingly depend on AI-driven risk scoring at the point of authentication to differentiate real fraud from normal customer behavior in real time. The goal is simple: stop bad transactions while letting good buyers checkout with as little friction as possible.

In ecommerce, 3D Secure 2(3DS2) supports this shift by enabling a strong, risk-based authentication model. Instead of depending on a single static signal, 3DS2 can share more context about the transaction and device, allowing issuers to apply machine learning to decide whether the shopper can be “frictionless approved” or needs a step-up challenge like a one-time passcode or bank app verification.

For CBD merchants, sending only suspicious transactions into step-up authentication keeps checkout smooth for real buyers while still reducing fraud and chargebacks.

That means higher approval rates, fewer abandoned carts, and lower dispute exposure without turning checkout into a confusing process.

Also Read: How to Create an Effective CBD Business Plan

4. AI for chargeback prevention: stopping disputes before they happen

Chargebacks are often more damaging than the actual fraud loss because they create long lasting consequences that go beyond a single transaction. Each dispute can negatively impact processor risk ratings, increase reserve requirements, and threaten long-term account stability especially for CBD merchants working in a higher-scrutiny environment.

Because of this, modern fraud strategies increasingly focus on preventing chargebacks before they ever occur.

AI-driven chargeback prevention works by identifying early signals that predict disputes, rather than reacting after the fact. One major area is friendly fraud prediction.

Machine learning models analyze historical patterns to learn which combination of behaviors like purchase timing, device signals, shipping choices, and customer history are most likely to cause “not authorized” or “item not received” claims. When these patterns appear the system can take proactive steps to reduce dispute risk.

Another important area is smarter order validation. Rather than treating all transactions the same, AI will apply targeted controls only where they matter.

For instance, AI can automatically apply signature-on-delivery to defined risk tiers, require delivery confirmation for higher-risk shipments, and add lightweight verification for SKUs with a history of disputes.

AI also plays an important role in descriptor and customer communication optimization. Many chargebacks happen because customers don’t recognize the merchant name or descriptor on their statement and assume the transaction is unauthorized.

AI systems analyze dispute data and recommend clearer billing descriptors, more detailed receipts, and timely post-purchase communications.

Improving descriptors, receipts, and post-purchase communication helps customers recognize charges immediately, which lowers avoidable disputes while keeping checkout exactly the same.

For CBD merchants, AI-powered chargeback prevention stabilizes approvals and processor relationships by catching dispute signals early, turning chargebacks into something that you can prevent and not just respond to.

Also Read: Why Do CBD Business Struggle With Payment Processing and How can They Fix it

5. AI + compliance monitoring: fraud prevention that also protects processor relationships

For CBD merchants, fraud prevention and compliance are interconnected because from a processor’s perspective, both create risk if they are inconsistently or poorly controlled.

That is why many CBD processors now expect compliance-first workflows, so AI is increasingly used to track and enforce those rules in real time instead of depending on manual reviews once after problems appear.

Modern payment providers integrate compliance controls directly into transaction flow.

Instances include SKU-level allowlists to ensure only approved products are sold, THC-threshold checks based on product classification, and geolocation rules that block restricted transactions or shipping regions.

Automating these controls prevents accidental violations without slowing compliant checkouts, while AI continuously monitors product, transaction, and behavior patterns to catch risks early.

AI can flag risky listings early, detect sudden spikes in restricted or borderline products, and spot pattern shifts that indicate policy workarounds rather than genuine demand.

Instead of reacting to processor inquiry or account review, merchants can address issues proactively. This matters because compliance issues often seem like fraud issues to banks. It increases uncertainty, unpredictability, and operational risk.

A sudden surge in restricted products, inconsistent SKU classification, or unexplained geographic activity can increase the same warnings as actual fraud even if no criminal activity is involved.

AI-driven compliance monitoring helps reduce that uncertainty. By keeping product catalogs, transaction flows, and regional rules aligned in real time, merchants demonstrate consistency and control to processors.

For CBD businesses, this not only reduces fraud and dispute exposure, but also strengthens processor relationships, reduces the chances of account reviews, and supports long-term stability in a tightly regulated payment environment.

6. AI and ACH/pay-by-bank: preventing fraud beyond card rails

As CBD merchants look beyond cards, many adopt ACH, direct debit, and pay-by-bank for wholesale, B2B, and high-value orders to support larger payments and lower costs.

While these methods can lower processing costs and enable bigger orders, they come with a different set of fraud risks and compliance requirements that must be managed separately.

ACH fraud does not follow the same patterns as card fraud, and expectations around risk management are defined by Nacha rules rather than card network standards.

Nacha has emphasized stronger account validation and fraud detection responsibilities for online (WEB) debits, particularly around validating consumer bank account information at first use.

It has also highlighted the need for risk-based processes to identify potentially fraudulent ACH activity, placing more accountability or originators to monitor and control return rates, unauthorized debits, and abnormal transaction behavior.

AI helps CBD merchants meet these expectations without depending on rigid, manual controls. One powerful application is spotting first-use account warnings, like inconsistencies between the bank account data, the device fingerprint, and the way the transaction behaves.

Over time, machine learning can evaluate bank account risk by analyzing behavioral trends, transaction frequency, and sudden changes that may indicate account misuse or synthetic identity activity.

For merchants handling higher volumes or larger payment files, AI can identify unusual batch behavior like sudden shifts in file size, timing, or return patterns before they escalate into operational issues.

Proactive AI monitoring can keep ACH return rates under control by avoiding bank reviews and gives CBD merchants strong fraud protection across pay-by-bank channels and not just cards.

It supports compliance with Nacha requirements, protects banking relationships, and enables lower-cost payment methods to scale while keeping the experience smooth for legitimate customers and partners.

Conclusion

AI is transforming CBD fraud prevention by replacing rigid blanket rules with real-time, context-aware risk decisions that protect revenue while keeping legitimate buyers flowing smoothly through checkout.

Rather than broadly applying blocks or friction, AI evaluates risk in real time using behavior, transaction context, and historical signals to separate legitimate customers from actual fraud.

This lets CBD merchants safeguard revenue while keeping approval rates high and the customer experience smooth.

Because CBD is closely monitored by banks and processors, AI supports more than fraud prevention powering smarter authentication, chargeback reduction, and compliance monitoring to keep risk stable and predictable.

From routing only the right transactions into step-up verification to identifying dispute-prone orders before the shipment, AI helps merchants stay aligned with processor expectations while reducing operational strain.

Just as important is trust, responsible AI use through data minimization, fairness monitoring, and clear customer communication ensures that security feels protective rather than intrusive.

This matters in CBD, where many customers are purchasing for the first time and are sensitive to anything that feels unusual or suspicious during checkout.

Ultimately, AI-driven fraud prevention enables CBD businesses to grow confidently. By lowering false declines, reducing disputes, and reinforcing compliance, AI turns fraud management into a strategic advantage supporting long-term stability, stronger processor relationships, and a smoother buying experience for legitimate customers.

If you still have any query with how AI is changing fraud prevention in CBD transactions then you may write to us at CBD Merchant Solutions and we are more than happy to assist you.

Frequently Asked Questions (FAQs)

1) Can AI reduce false declines for CBD merchants?

Yes. AI looks at context like device signals, behavior, purchase history, and checkout patterns so it can approve more legitimate orders while still preventing fraud and improving conversion rates.

2) Does AI help with chargeback prevention too?

Yes. By catching warning signals early, AI helps you hold, verify, or cancel risky orders before they become disputes, keeping chargebacks low and protecting processor relationships.