The fast growing CBD industry offers immense opportunities for entrepreneurs, but it also has significant compliance challenges particularly around payment processing and adhering to the 0.3% THC threshold.

The 2018 Farm Bill serves as the legal boundary which separates hemp-derived CBD from marijuana in the United States.

Any product which exceeds 0.3% delta-9 THC on a dry weight basis will be categorized as marijuana, which causes serious legal, financial, and processing complications.

For CBD merchants, staying compliant is not just about following regulations; rather it is essential to maintain trust with payment processors, banks, and customers.

For CBD merchants, staying compliant is not just about following regulations, it’s the key to maintaining trust with payment processors, banks and customers.

The CBD market is classified as a high-risk category, due to which traditional financial institutions proceed carefully and impose stricter requirements on merchants.

Even small compliance mistakes such as inaccurate labeling, inaccurate lab reports or unclear THC testing documentation can cause frozen payments, account closures, or increased regulatory assessments.

In such an environment, understanding the CBD payment compliance landscape is essential for long-term success.

Through this blog we will walk you through the fundamentals of CBD payment compliance and explain the importance of strictly maintaining the 0.3% THC limit to ensure legal operation and financial stability.

We will explore everything CBD entrepreneurs must know to remain compliant which includes federal and state regulations, merchant account requirements, lab testing procedures, and essential regulatory best practices.

You will also learn how to avoid chargebacks, reduce risk, and develop a credible reputation with payment providers.

So if you are launching a new CBD brand or expanding an existing CBD brand, understanding THC compliance and CBD payment processing protects your business which becomes the foundation for long-term, sustainable growth in a strongly regulated industry.

Also Read: Comparing CBD Payment Gateways

Legal & Regulatory Background

1. Federal Frameworks (U.S. Example):

The 2018 Farm Bill made the cultivation and sale of hemp legal, classifying cannabis which contains no more than 0.3% delta-9 THC on a dry weight basis.

Though hemp and hemp derived CBD products with less than 0.3% THC are federally legal but are closely regulated under federal and state laws.

The U.S. The Department of Agriculture(USDA) through the Agriculture Marketing Service(AMS) along with state agencies, tracks hemp licensing, production, and compliance.

But the legalization comes with important restrictions, as the Food and Drug Administration(FDA) continues to regulate the use of CBD in foods, supplements, cosmetics, and all product marketing claims.

So, businesses cannot legally promote CBD products as medical treatments or therapeutic remedies without FDA approval to ensure public safety and compliance with federal laws.

Also Read: is CBD Legal in all 50 States

2. Hemp vs. Marijuana – The 0.3% Distinction:

The 0.3% THC limit legally differentiates hemp from marijuana. While hemp containing 0.3% or less delta-9 THC is federally legal, while anything exceeding that limit is classified as marijuana and remains strongly controlled.

For CBD merchants, exceeding the 0.3% THC limit often causes regulatory violations, frozen merchant accounts, loss of payment processing privileges, and possible legal action under federal or state law.

Also Read: The Best Marijuana Marketing Strategies

3. Enforcement, Oversight & Discretion:

The USDA regulates hemp production, but enforcement may differ particularly during laboratory certification and the disposal of crops that exceed legal THC limits.

DEA-authorized laboratories perform THC testing, whereas state agencies oversee grower compliance, recordkeeping, and reporting to maintain alignment with federal hemp standards.

As rules keep changing, merchants must remain proactive and informed to adapt to changing oversight, inspection practices, and enforcement priorities within the hemp industry.

Also Read: Marketing Ideas for CBD Business

4. State & International Variation:

In the U.S. hemp regulations differ by state, with some enforcing more strict limits, broader THC testing that includes total THC, or detailed labeling and product restrictions.

On an international level most of the countries set the threshold at 0.25 THC or less. Businesses involved in international trade must comply with each place’s specific legal and import requirements.

Businesses involved in global trade must comply with each place’s specific legal and import requirements.

Merchants selling in different regions must always adhere to the most strict applicable regulations to ensure full compliance and avoid legal or financial penalties.

Also Read: Best Ecommerce Platform for CBD

5. Measurement & Dry Weight Basis:

“Dry weight basis” refers to measuring the concentration of a substance in this case, Delta-9 THC after all the moisture has been removed. It does matter because water content can differ and by removing it you have a consistent measure of the actual material, allowing for accurate comparisons between samples.

Also Read: Why CBD Business are Considered High-Risk

6. Testing Standards, Uncertainty & Lab Practices:

Implementing the right testing is crucial. Labs use methods like gas chromatography or liquid chromatography to test cannabinoids. While every method has measurement uncertainty, labs must validate methods, maintain calibration, and follow standard operating protocols.

Inaccurate testing can occur because of improper sampling, contamination between batches, or uncalibrated equipment, causing compliant hemp to be wrongly classified as noncompliant.

Due to such uncertainties, many companies build safety margins which target a THC level well below 0.3% creating a safety margin that reduces the risk of compliance failures because of lab inconsistencies or testing errors.

Also Read: How Much Does an Average CBD Store Make

7. Risks of Over-Limit Products:

When a batch exceeds 0.3% THC limit, then it is classified as noncompliant and may face seizure, destruction, or legal consequences. This can also threaten a merchant’s relationship with payment processes such as violations that are often treated as contractual breaches.

On top of that, products that later test above the threshold limit will be labeled as misbranded which causes consumer complaints, damaging brand credibility, and causing regulatory scrutiny, fines, or litigation which can severely impact business operations and reputation.

Also Read: Selling CBD Products Online

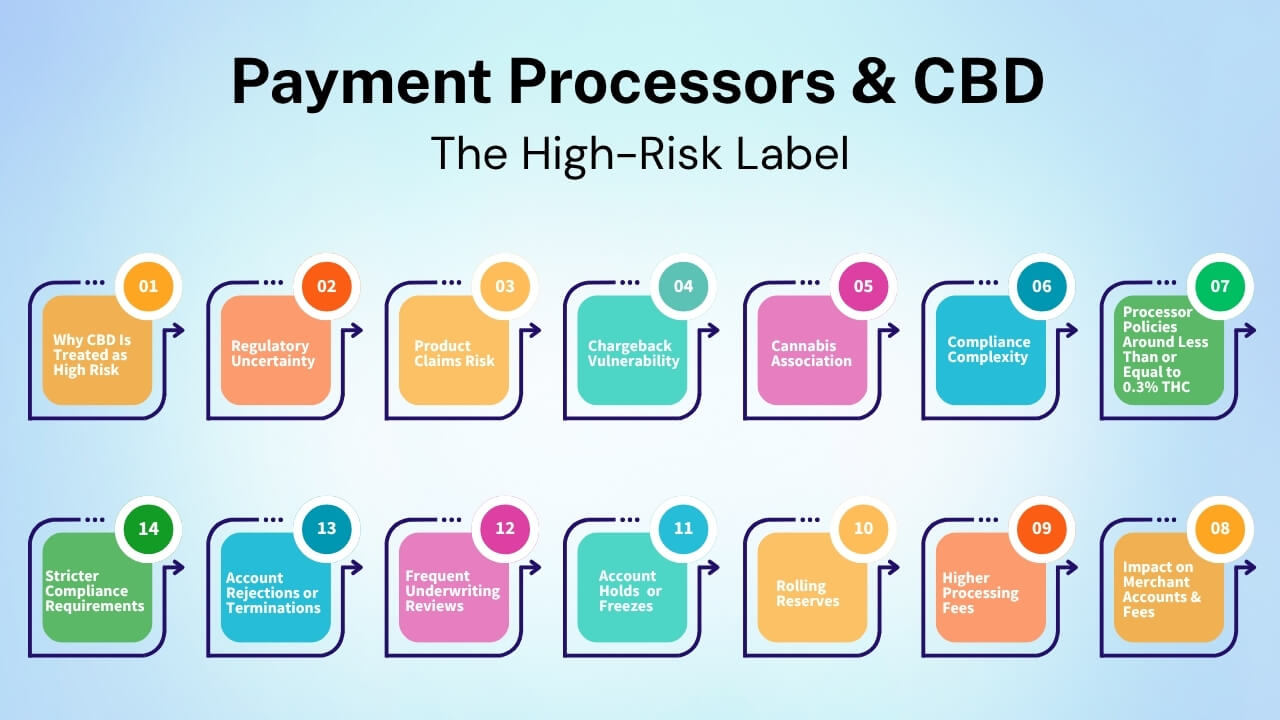

Payment Processors & CBD — The High-Risk Label

1. Why CBD Is Treated as High Risk:

Even when a CBD product is within legal THC limits which means it contains less than 0.3% THC, still many payment processors classify CBD merchants as high risk.

This classification is because of legal complexities, reputational concerns, and financial exposure within the industry. So it is essential for processors to protect them from chargebacks, fraud, and violations of banking or federal laws.

As a result, CBD merchants often face higher processing fees, stricter underwriting, and continuous monitoring. Below are five key reasons why CBD remains high risk.

Also Read: What is High-Risk Merchant Account

2. Regulatory Uncertainty:

Federal and state laws governing CBD keep evolving. Inconsistent enforcement and unclear FDA guidelines make payment processors cautious about possible future restrictions or fines.

Also Read: How to Expand Your CBD Business to New Market

3. Product Claims Risk:

Many CBD businesses market their products with health or wellness claims. These claims can lead to FDA or FTC investigations and may result in fines, refund obligations or chargebacks when consumers believe that they were misled.

Also Read: Understanding Chargebacks in CBD Industry

4. Chargeback Vulnerability:

Customers may initiate disputes because of unclear product expectations, dissatisfaction with results, or delivery platforms, causing financial losses for processors.

Also Read: How to Avoid Frauds and ChargeBacks in CBD Industry

5. Cannabis Association:

CBD originates from legally grown hemp, while its association with cannabis continues to influence public perception and financial policies, leading many banks to treat the industry with increased caution.

Also Read: How to Market Cannabis

6. Compliance Complexity:

CBD merchants are required to maintain strict documentation standards like Certificates of Analysis(COAs), business licenses, and clear labeling compliance which create administrative burdens and risk of disqualification for even small compliance errors.

Also Read: How to Get a CBD License

7. Processor Policies Around less than or equal to 0.3% THC:

Payment processors maintain strict oversight of less than or equal to 0.3% THC rule, often requiring Certificates of Analysis, batch testing, or third-party verification to prove compliance.

For instance, Square permits CBD sales only for hemp-derived products within this threshold. Processors like KORONA POS by COMBASE also ban medical claims and suspend accounts for violations.

Also Read: How to Protect Your CBD Business from Payment Processor Shutdowns

8. Impact on Merchant Accounts & Fees:

As CBD is classified as a high-risk industry, merchants face stricter account management and increased costs from payment processors.

This increased risk perception can affect cash flow, account stability and long term relationships with payment providers.

Also Read: How to Get a Merchant Account for CBD Business

9. Higher Processing Fees:

CBD merchants are often charged higher processing rates in order to compensate processors for the greater financial and regulatory risks associated with the industry.

Also Read: Understanding CBD Payment Terms

10. Rolling Reserves:

So processors may withhold a percentage of sales for a certain duration in order to protect against chargebacks, refunds, or compliance-related issues.

11. Account Holds or Freezes:

Processors may temporarily restrict access to funds if they detect compliance issues, unusual transaction activity, or an increase in chargebacks.

12. Frequent Underwriting Reviews

Regularly payment processors re-evaluate CBD merchants to ensure constant compliance with changing regulations and changes in business risk.

13. Account Rejections or Terminations:

While mainstream financial institutions decline or close CBD merchant accounts due to legal uncertainty and increased compliance risks.

14. Stricter Compliance Requirements:

To keep their payment processing active, CBD merchants must continually prove regulatory compliance, product transparency, and full legal adherence.

Also Read: CBD Industry Trends Challenges and Future Outlook

Best Practices for Staying Compliant (with payments in mind)

1. Rigorous Lab Testing & Certificates of Analysis (COAs)

Each product lot should be tested by trusted, accredited third-party laboratories . Each SKU must have a detailed Certificate of Analysis (COA) confirming THC content, full cannabinoid profile, product purity, and absence of contaminants such as pesticides and heavy metals.

COAs should be easily accessible to consumers ideally through QR codes and securely stored for internal compliance records. To prove traceability COAs must match the batch and lot number on the label.

2. Chain of Custody, Sample Retention & Record-Keeping:

It is essential for CBD merchants to maintain documentation showing how samples were collected, stored, transported, and tested. Also retain sample portions from each batch for quality checks and securely store all testing records for several years as required by regulatory authorities or payment processors. Ensure that every step from sourcing to production is documented.

Also Read: How to Choose the Right CBD Merchant Account

3. Labeling, Packaging & Declaring THC Levels:

Labels should clearly provide the tested THC content, batch or lot number, net weight, and all required disclaimers and warnings as per regional laws.

Use tamper-evident packaging to protect consumer safety, preserve product integrity, and clearly show the contents were not changed after manufacturing.

Use clear, accurate, and compliant language on labels to prevent confusion and ensure consumers fully understand the product’s contents and intended use.

If specific symbols or icons like cannabis warning marks are required by law then it should be displayed accurately and meet all legal design and placement standards for full regulatory compliance.

Also Read: How to Start a CBD Dispensary in California

4. Restricting Risky SKUs / Removing High-THC Types:

To reduce compliance risks, restrict or remove high-THC product types like raw flower or concentrates which show greater variability in testing. Exclude SKUs that frequently approach the THC threshold, and guide customers toward safer alternatives like broad spectrum or isolate formulations which maintain quality while ensuring consistent regulatory compliance.

Also Read: How Fast Payouts Can improve Your CBD Business CashFlow

5. Transparency in Marketing & Avoiding Health Claims:

Avoid making medical claims for instance “cures anxiety”, “treats pain” unless the product is FDA-approved for such use. The FTC regularly enforces actions that include warnings and fines against companies which make unverified or misleading health claims about their products.

Must use only allowed health or wellness claims for your region, and also add clear disclaimers that support any statements with valid scientific proof when possible.

Also Read: The Ultimate Guide of CBD Social Media Marketing in 2025

6. Working with CBD-Friendly Payment Providers:

Select payment processors which openly support CBD businesses which can provide written proof of their CBD-compliance policies. Such specialized providers better understand regulatory risks and offer long-term stability.

During underwriting, be prepared to provide Certificates of Analysis(COAs), business licenses, and detailed product documentation to verify compliance and reduce approval delays.

Also Read: How to Choose the Best CBD Payment Processing Company

7. Communication & Documentation with Banks:

Keep open communication with your acquiring bank or payment processor to build trust and ensure transparency. Inform them immediately about any new or modified products, and provide updated documentation as required.

If audits or information requests occur, provide Certificates of Analysis(COAs), batch records and detailed compliance processes to demonstrate full regulatory adherence.

Maintaining transparency builds trust with processors and helps prevent unexpected account holds or terminations.

Also Read: Why Traditional Banks Reject CBD Merchant

Risk Mitigation & Chargeback Prevention in the CBD Context

1. Compliance as Dispute Prevention:

Strong compliance is not just a legal protection rather it’s an effective strategy for preventing disputes and chargebacks. By showing their CBD products are lab-tested, under 0.3% THC, accurately labeled, and sold transparently in full compliance, merchants strengthen credibility and improve chargeback or customer dispute.

Most chargebacks in the CBD industry are due to customer confusion regarding legality, labeling, or product effects. So it is important to maintain communication clear, proper documentation, and strictly adhere to testing and labeling standards to reduce such misunderstandings.

It is only by regularly operating within legal boundaries and maintaining detailed documentation that helps merchants to maintain their credibility strongly and reduce costly chargebacks or account issues.

Also Read: How to Expand Your CBD Business to New Market Without Payment issue

2. Fraud Controls, Authentication & Risk Scoring:

Implementing strong fraud prevention tools is important for protecting CBD transactions and maintaining processor trust. Use Address Verification Service(AVS) checks, CVV verification and velocity limits to find unusual purchase patterns.

Geolocation and device fingerprinting helps to find mismatched data or high-risk locations. While multi-factor authentication and 3D Secure makes transaction security strong by ensuring the identity of the cardholder through additional verification steps before payment approval.

While combined with an automated risk scoring system, such measures help to find fraud activity in real time reducing chargebacks and protecting both merchants and customers. Proactive fraud prevention not just improves security but also makes long-term payment stability strong.

Also Read: Why CBD Business Struggle With Payment Processing and How Can They Fix it

3. Clear Billing Descriptors, Receipts & Product Details:

One of the simplest ways to avoid disputes and chargebacks is a clear and recognizable billing descriptor. Instead of using unclear or coded names, use something which customers will instantly recognize.

It is essential that you provide detailed receipts and order confirmations that include product names, prices, and contact information for customer support.

Ensure you provide detailed product information on your website. Also send confirmation emails with ingredients, usage guidelines, links to Certificates of Analysis and valid disclaimers in order to maintain transparency and compliance.

Only when customers understand what they purchased that they are able to verify product authenticity, confusion due to which refund request decreases. By maintaining transparent communication helps to build trust, strengthens compliances and promotes long-term customer satisfaction.

Also Read: CBD POS Systems 7 Must have Features for dispensaries

4. Shipping, Delivery Tracking & Communication:

With reliable shipping practices and proactive communication are crucial to reduce customer disputes and maintain customer trust. Also provide tracking numbers and real-time updates through which customers can easily monitor their shipments.

While in case of higher-value or sensitive CBD products require a signature from customers upon delivery to confirm receipts and reduce claims for non-delivery. Because if there is a delay, damage, or issue then contact the customer immediately with a clear explanation and resolution plan.

Only a proactive approach helps prevent frustration from converting into refund requests or chargebacks. Maintain detailed shipping records which include carrier details and delivery confirmations which will help to resolve disputes if necessary.

With consistent and timely updates during the delivery process helps build customer trust, and improve overall confidence in your brand.

Also Read: CBD Email Marketing Campaign Guide

5. Refund & Cancellation Policies Customized to CBD:

Ensure you develop clear, fair, and transparent refund and cancellation policies that show customer satisfaction goals and CBD-specific regulations.

Where some regions restrict returns of consumable hemp or CBD items clearly defining which products are eligible for refunds or exchanges and specify timelines for submitting such requests.

It is important that you show your policy on your website, checkout page, and order confirmations to avoid confusion. Also encourage customers to contact your support team directly for assistance before filing disputes with their bank as resolving issues internally is faster and avoid chargebacks.

Provide responsive customer service and clear communication regarding refund status. While well-defined, legally compliant policies help build credibility, protect your business from financial risk and make customer trust stronger for your brand in the long run.

Also Read: How to Advertise CBD Brand in the Best Possible Manner

6. Internal Audits & Dashboards:

It is crucial to establish regular monitoring and internal audit systems to maintain compliance and operational integrity. So implement data dashboards that track key performance and compliance metrics like THC test results, batch variances, refund and return rates, disputes, and chargeback reasons.

Such dashboards provide real-time insights that help you identify compliance risks early and address them quickly before they turn into regulatory issues.

Conduct regular audits to verify that all documentation that includes Certificates of Analysis(COAs), product labels, and testing records which remain up to date and also match with legal standards.

While reviewing sales, shipping, and customer feedback data to find emerging risks or quality concerns. And when deviations or noncompliance are found, apply corrective actions at the right time, document remediation steps, and retrain staff if necessary.

Regular monitoring makes sure you maintain transparency, reduces financial exposure, and reinforces consumer trust.

Also Read: Best Website Builders for CBD Business

7. Handling Nonconforming Batches:

When a batch tests above the legal 0.3% THC threshold then it is essential to develop a proper remediation plan in order to remain compliant and maintain trust.

Based on local regulations, it might be required to recall, reblend, destroy or do a remediation extraction to bring THC levels in legal limits.

It is important that you always verify local rules as some regions allow remediation or isolation while in other regions complete destruction of the noncompliant material is compulsory.

And every step of the process like test results, corrective actions, and disposal records should be rigorously documented.

Also maintain written evidence regarding destruction or remediation for regulatory audits and processor reviews. Such records work as proof of good faith compliance during an audit or regulatory scrutiny.

On top of that, evaluate your cultivation, extraction, and sourcing processes to find why THC levels exceeded the limit and implement preventive measures.

Because proactive handling of nonconforming batches reduces risk, protects reputation, and ensures continued operational approval.

Conclusion:

The 0.3% THC rule is the legal boundary that differentiates marijuana under the 2018 Farm Bill. For CBD businesses it is crucial to stick to the 0.3%THC limit which is not just about being lawful but also a pre-requirement for maintaining access to payment processors, banking, and distribution channels.

If the CBD products exceed the 0.3% Delta-9 THC then it will be categorized as marijuana as per federal law that can cause penalties, product recalls, or even loss of merchant accounts. To remain compliant, CBD producers and retailers must implement testing and documentation protocols.

It is crucial that every batch should be verified by well-authorized third-party laboratories to ensure that THC levels are within legal limits. Maintain detailed certificates of analysis(COAs) and make them accessible to regulators and consumers to show transparency and good faith.

And also proper labeling, tracking, and recordkeeping are equally important to prevent misbranding issues and ensure full compliance with regulatory standards. As the CBD industry operates in a high-risk category, payment processors, card networks, and banks closely monitor compliance.

And even if a single noncompliant batch is found then it may lead to account freezes, or permanent account termination. On top of that, THC limits differ by state and on global levels so businesses who are planning to expand or export must understand local requirements before shipping products.

Being in this ever changing regulatory environment, maintaining constant awareness and adaptability is crucial to ensure continuous compliance and business stability.

So conducting regular audits, providing staff training and working closely with legal and compliance professionals are crucial steps to maintain constant regulatory adherence.

It is only by maintaining strict quality control and transparency that CBD Merchant Solutions can protect and sustain consumer trust.

Frequently Asked Questions (FAQs):

1. What happens when a CBD batch tests above 0.3% THC?

Whenever a batch tests above the 0.3% THC then those batches must be either recalled, destroyed, remediated, or reprocessed based on the local regulations. While all corrective actions and disposal records should be carefully documented.

2. How often should CBD businesses test their products?

Regular testing for at least for once per production batch is recommended. Additionally spot checks and third-party verifications help ensure consistency and show good faith to regulators and financial partners.